What is share warrant?

There is no typical definition available for Share Warrant in any statutory act. In layman’s language, Share Warrant is an option issued by the business enterprises, wherein the warrant holder has a right to subscribe equity stocks at a pre decided rate on or after a pre decided time period.

As per Section 2(h) of Securities Contract Regulation Act, 1956, Securities include:

- shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate

- derivative

- units or any other instrument issued by any collective investment scheme to the investors in such schemes

- security receipt as defined in clause (zg) of section 2 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

- units or any other such instrument issued to the investors under any mutual fund scheme

- Government securities

- such other instruments as may be declared by the Central Government to be securities and

- rights or interest in securities.

Since the underlying instrument in warrants is equity shares which in turn are marketable securities, it is far apparent that warrants will also be marketable in nature. Further, the Reserve Bank of India vide Notification No. FEMA. 308/2014-RB2, dated June 30, 2014, has clarified that warrants shall be treated as security within the meaning of Section 2(za) of FEMA. It can be inferred here that Share Warrants are one of the type of Securities offered by business entities.

A noteworthy fact here is that warrants and options are similar to the effect that both the contractual financial instruments allow the holder, special rights to buy securities. Both are discretionary and have expiration dates. They differ mainly in respect that options can be issued only to the employees of the company whereas warrants can be issued to a much wider range of people. Also, there are certain restrictions on issuance of options in terms of the provisions of SEBI (Issue of Capital and Disclosure Requirement) Regulations, as compared to issuance of Warrants.

For better understanding of the concept of Share Warrant, let’s take an example:

ABC Limited issues warrant for 10000 shares convertible into equivalent number of Equity Shares of the Company, to its directors, at a price of Rs. 10 per Equity Share of the Company or such other price as may be determined in accordance with the provisions of applicable laws, and subject to a lock-in period of 18 months from the date of issuance.

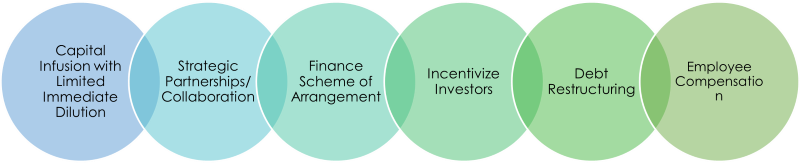

Rationale of Issuing Share Warrants:

Companies issue Share Warrants for various reasons, wherein Companies can leverage these benefits to support growth initiatives, enhance financial flexibility and create value for shareholders and stakeholders over the long term.

Conditions to Issue Share Warrants:

Companies can issue Securities including Share Warrants through private placement or preferential allotment by complying with the provisions of Section 23, 42 and 62 of the Companies Act, 2013. Companies are required to fulfil a few conditions before issuing share warrant:

- Under Companies Act, 2013:

- Authorization by the Articles of Association

- Pass Board Resolution for issuance of warrants

- Pass Special Resolution for issuance of warrants

- File Return of Allotment in PAS-3, within 30 days of allotment

- Price of the shares or other securities so issued on preferential basis, is determined on the basis of valuation report of the Registered Valuer

- Under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018:

- All Equity Shares held by proposed allottees are in dematerialized form

- Issuer complies with the conditions for continuous listing of Equity Shares

- Obtain PAN of proposed allottees

- Obtain In-Principle Approval from Stock Exchange(s) where its Equity Shares are listed

- Tenure of Convertible Securities shall not exceed 18 months from the date of allotment.

- All Equity Shares allotted by way of preferential issue shall be made fully paid up at the time of allotment

Procedure for Issue of Share Warrants:

- Steps at the time issue of warrants-

- Authorization by the Articles of Association

- Check Authorized Capital in Memorandum of Association

- Pass a Board resolution in a duly convened Board Meeting for issuance of share warrants

- Obtain Valuation report from a Registered Valuer, for pricing of the underlying shares

- Convene a General Meeting of its members to pass a special resolution for approving the proposal of issuance of share warrants, as recommended by the Board

- File Form MGT-14 and GNL-2 for filing of resolutions with the Registrar of Companies

- Issue offer letter to proposed allottees for share warrants

- Board Resolution allotment of warrants

- Obtain In-Principle Approval from Stock Exchange(s) where its Equity Shares are listed (In case of Listed Entity)

- Receipt of allotment request from proposed allottees

- At least 25% of the consideration amount, based on the exercise price, must be received upfront at the time of allotment of warrants

- Pass a Board resolution in a duly convened Board Meeting for allotment of warrants convertible into equity shares

- The tenure of Convertible Securities shall not exceed 18 months from the date of allotment of warrants

- Steps at the time Conversion of warrants-

- Company shall pass a Board resolution in a duly convened Board Meeting for allotment of share or other securities, as the case may be pertaining to issue of Share warrants

- File return of Allotment in Form PAS-3 with the Registrar of Companies

- Make relevant entries in the Register of Members

- Obtain Listing Approval from Stock Exchange(s) where its Equity Shares are listed (In case of Listed Entity)

Incidence of Taxation of Share/ Stock Warrants:

The incidence of taxation on Share Warrants can vary depending on several factors, including the jurisdiction’s tax laws, type of warrant and specific circumstances of the transaction. Here are some common incidences of taxation on Share Warrants:

Exercise of Warrants

Sale of Warrants

Sale of Shares Acquired

Conversion of Warrants into Shares

Conclusion:

Companies can raise capital from their current shareholders through the use of special financial instruments called share warrants. Share warrants offer a simpler and more affordable means of obtaining capital than public offerings. Because they allow current shareholders to buy additional firm shares at competitive rates, share warrants are also advantageous to them.

In spite of the fact that numerous companies issued them some time recently the Companies Act of 2013 came into constrain, the hone has since dwindled. In any case, in the event that one is a speculator with a warrant, one has to be careful to work out them at right time. Working out a warrant when the stock cost is unfavourable to an individual can lead to a misfortune. On the other hand, in case the holder does not arrange on working out the warrant, at that point they can consider offering it on the auxiliary advertise rather than letting it pass so that they can advantage from instrument.

Disclaimer

The information provided in this article is intended for general informational purposes only and should not be construed as legal advice. The content of this article is not intended to create and receipt of it does not constitute any relationship. Readers should not act upon this information without seeking professional legal counsel.