Introduction

Australia’s Tax System is regulated by a wide range of laws and rules intended to raise money for the government and pay for public services. The Australian Taxation Office (ATO), being the regulatory authority, has imposed different taxes for different taxpayers. The imposition of high tax rates among the most developed nations, at a flat rate of 30% for large corporations and a reduced tax rate of 25% for small and medium-sized enterprises, has diminished the benefits of doing business in Australia. However, despite having the most complex taxation regime, Australia has the highest growing business rate in Asia Pacific for adapting to the dynamic business environment. Hence, this article provides an insight into the Australian Taxation Laws that are in force on Business Corporations.

Legal Obligations for Corporations as Taxpayers

Business Registration Requirements

Income earned in Australia is subject to taxation, but business corporations with a permanent location inside Australia’s territorial jurisdiction must register in order to facilitate communication with all tiers of government. To conduct business in Australia, you must have the following registrations:

- Australian Business Number (ABN) – This is a unique 11-digit identifier to recognize the business by the government and streamline the corporation for tax reporting, invoicing, and easy interaction with other government agencies for tax purposes. It is applied online using the Australian Business Register. This unique identification is useful in many ways:

- Allows businesses to operate in Goods and Services Tax (GST) and claim GST credits.

- Confirms the business identity with others while placing orders or invoicing.

- Simplifies dealings with third parties as they can search to verify the business status using the ABN.

- Ensures that the business is legally recognized by the government while giving it a legal identity.

- Provides access to online government services.

- Australian Company Number (ACN) – This registration requirement is necessary for setting up a company that is (Pty Ltd.) and is distinct from the ABN as the ACN is used for corporation identification and the ABN is used for taxation reporting purposes. ASIC (Australian Securities and Investments Commission) registration plays a crucial role in GST (Goods and Services Tax) operations for smooth reporting. Moreover, it streamlines corporate taxation reporting for lodging tax returns and payments.

Australia’s Tax Compliance and Obligations

- Goods and Services Tax (GST)

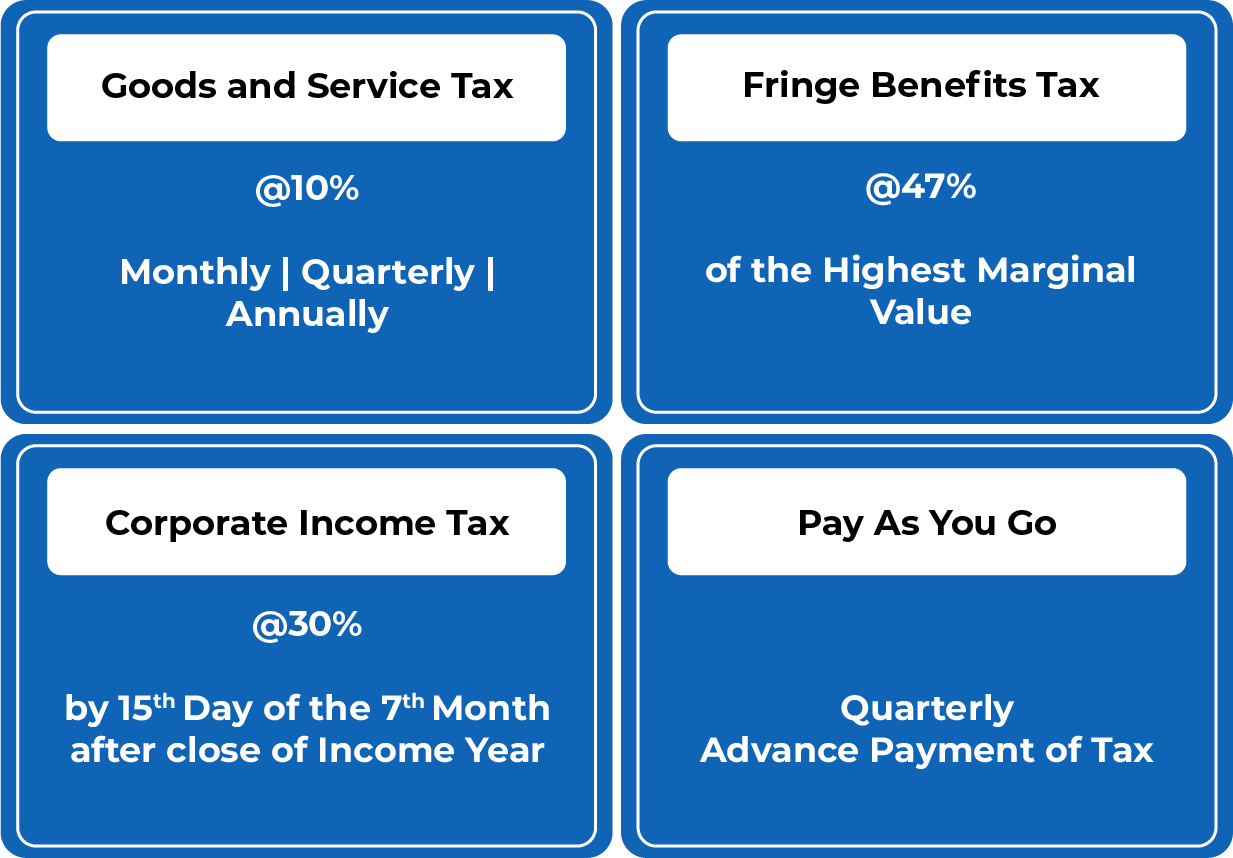

GST, governed by Goods and Services Tax Act 1999, is levied on the supply of goods and services at a flat rate of 10% on every person whose annual turnover exceeds AUD $75,000. It is a multilevel tax on items consumed or sold in Australia. Business corporations registered under GST charge the tax on the price of goods and services and pay it to the Australian Taxation Office.

Filing and payment of GST can be done Monthly, Quarterly, or Annually. Business entities can file and pay their GST return monthly if their turnover is AU$20 million or more, by the 21st day of the month preceding the end of the reporting period. Quarterly filing and payment are to be made by the business by the 28th of the following month in which the quarter ends, if the turnover is between AUD $75,000 and AU$20 million. Annual filing and payment are due by the 28th of February of the following year if the turnover is under AU$75,000, or for those who voluntarily elect to get registered under Australian Goods and Services Tax. - Corporate Income Tax (CIT)

CIT, governed by Income Tax Assessment Act 1997, applies to corporations that have a Permanent Establishment in Australia or derive income sourced in Australia. It is imposed at a flat rate of 30% for corporations with an aggregate turnover threshold of AU$50 million or more, and 25% for corporations with an aggregate turnover threshold of less than AU$50 million. The due date for filing the Annual Income Tax Return is the 15th day of the 7th month after the close of the income year. - Pay As You Go (PAYG)

PAYG refers to the regular prepayment of taxes in installments to reduce the tax liability at the end of the income year. PAYG is divided into two distinct categories:- PAYG Withholding

- PAYG Instalment

PAYG Instalment is a tax obligation that is estimated or paid in advance for the income earned by corporations.

PAYG is also optimized by businesses that file a Quarterly Business Activity Statement (BAS) under Goods and Services Tax.

Hence, PAYG has created a consistent regular payment of tax in Australia, which reduces the tax burden at the end of the income year by spreading payments across the year. - Fringe Benefits Tax (FBT)

FBT is a tax on the benefits provided to employees by employers. The tax is levied on the value of the annual benefit given to an employee and is paid by corporations contributing to the welfare of their employees. It is calculated at the rate of 47% of the highest marginal tax rate the employee would have to pay on their own income.

Obstacles in Taxation Compliance for Australian Businesses

The Australian Taxation System plays a significant role in raising revenue for the state and ensuring the smooth functioning of the economy. However, being one of the most robust taxation regimes among developed nations, it presents challenges for businesses and individuals due to its complexity and compliance requirements.

Australia levies the highest tax rates on business income in the Asia Pacific region, making it challenging for companies to evaluate their profits due to the heavy tax burden.

This challenge is faced by most businesses in Australia, particularly those paying Goods and Services Tax (GST). It is a consumption-based tax levied at multiple levels, which complicates record-keeping and compliance.

Another challenge for businesses is the need to pay multiple taxes, including Corporate Income Tax, Capital Gains Tax, Fringe Benefits Tax, and others. This increases administrative burdens and complicates compliance.

The emergence of e-commerce and the digital economy has made it increasingly complex for businesses to record digital transactions for GST purposes, particularly with cross-border transactions. This has created challenges in complying with tax obligations.

Possibilities for Reform

As observed in the previous sections, the dynamic business environment with increased globalization and digitalization, combined with the complex taxation system in Australia, may limit investment and growth opportunities. The country’s taxation system was built in a different era, and it is necessary for the government to simplify the federal tax system to enhance job opportunities, capital, and investment for future economic growth.

Reform may require courage, but the results could be rewarding with increased productivity and growth in the economy.

Conclusion

From the details provided in this article, it can be concluded that the Australian Taxation System is robust and involves stringent laws that may hinder growth and innovation in the economy. Therefore, it is suggested that tax laws and regulations need reforms that align with the dynamic business environment, addressing the challenges faced by corporations and business entities.

Disclaimer

The information provided in this article is intended for general informational purposes only and should not be construed as legal advice. The content of this article is not intended to create and receipt of it does not constitute any relationship. Readers should not act upon this information without seeking professional legal counsel.